Implementation of e-Invoicing in Malaysia: A Comprehensive Guide

Introduction to e-Invoicing

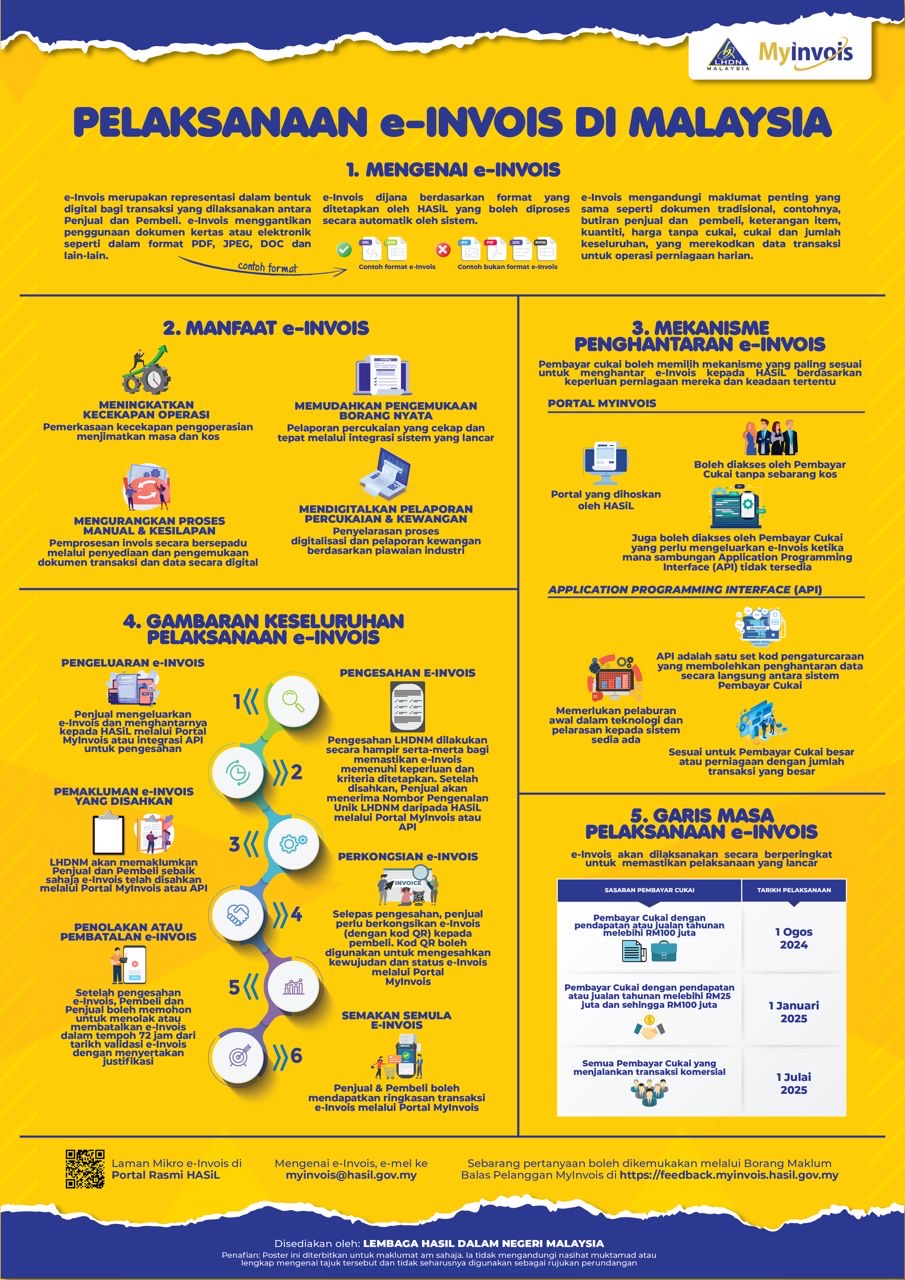

e-Invoicing, or electronic invoicing, represents the digital format of invoices used for transactions between buyers and sellers. This system replaces traditional paper invoices with digital formats such as PDF, JPEG, DOC, and more. In Malaysia, e-Invoices follow a specific format set by the Inland Revenue Board of Malaysia (HASiL), allowing for automatic system processing. This digital transformation helps streamline transaction documentation and daily operational tasks.

Benefits of e-Invoicing

Implementing e-Invoicing in Malaysia offers numerous advantages, including:

- Enhancing Operational Efficiency: e-Invoicing improves the speed of processing transactions, saving time and reducing operational costs.

- Simplifying Tax Reporting: It facilitates accurate and efficient tax reporting through seamless integration with reporting systems.

- Reducing Manual Processes: Automation of invoice issuance minimizes the need for manual data entry and paperwork, leading to fewer errors and quicker transaction processing.

- Digitizing Financial and Tax Reporting: Transitioning to digital financial and tax reporting enhances accuracy and reliability, ensuring compliance with industry standards.

e-Invoicing Transmission Mechanism

Taxpayers can choose the most suitable method to send their e-Invoices to HASiL based on their business needs and current technology infrastructure. The two primary methods are:

- MyInvois Portal: A portal provided by HASiL that allows taxpayers to send e-Invoices at no cost.

- Application Programming Interface (API): APIs facilitate direct and real-time transmission of e-Invoices from taxpayers’ systems to HASiL, ideal for larger taxpayers or businesses with high transaction volumes.

Overall e-Invoicing Implementation Process

The implementation of e-Invoicing involves several key steps:

- Issuance of e-Invoices: Sellers issue e-Invoices in the format specified by HASiL through the MyInvois portal or API for verification.

- Verification of e-Invoices: HASiL verifies e-Invoices in near real-time, confirming the details and authenticity.

- Announcement of Verified e-Invoices: Once verified, HASiL will announce the verified e-Invoice via the MyInvois portal or API.

- Rejection or Cancellation of e-Invoices: If an e-Invoice is rejected or needs to be canceled, it will be updated accordingly, ensuring accurate records.

- e-Invoice Sharing: After verification, e-Invoices are shared with relevant parties, including buyers and relevant tax authorities, ensuring transparency and compliance.

- Rechecking e-Invoices: Both sellers and buyers can recheck the transaction details via the MyInvois portal to ensure accuracy.

Timeline for e-Invoicing Implementation

The implementation of e-Invoicing will be carried out in stages to ensure a smooth transition for all taxpayers:

- 1 August 2024: For taxpayers with annual sales exceeding RM100 million.

- 1 January 2025: For taxpayers with annual sales between RM50 million and RM100 million.

- 1 July 2025: For all other taxpayers.

Conclusion

The transition to e-Invoicing in Malaysia marks a significant step towards digital transformation in financial transactions. By adopting e-Invoicing, businesses can benefit from enhanced efficiency, reduced costs, and improved accuracy in tax reporting. As Malaysia moves forward with this implementation, it is crucial for businesses to stay informed and prepare for these changes to ensure seamless compliance and operational efficiency.

“Learn about the implementation of e-Invoicing in Malaysia, its benefits, transmission methods, and the detailed process. Stay informed on the timeline and prepare your business for this digital transformation.”

Last Updated: March 2026

This guide has been updated to reflect the latest e-Invoicing implementation timeline announced by LHDN.

Latest Update on Malaysia e-Invoicing Implementation (2026)

Since the initial announcement of Malaysia’s e-Invoicing initiative, the Inland Revenue Board of Malaysia (LHDN) has provided additional updates and clarifications regarding the implementation timeline and compliance expectations.

The implementation continues to follow a phased approach based on the annual turnover or revenue of businesses.

Updated Implementation Timeline

The current rollout schedule is as follows:

01/08/2024 – Taxpayers with annual revenue exceeding RM100 million

01/01/2025 – Taxpayers with annual revenue between RM25 million and RM100 million

01/07/2025 – Taxpayers with annual revenue between RM5 million and RM25 million

01/01/2026 – Taxpayers with annual revenue up to RM5 million

Businesses with annual revenue below RM1 million are currently exempt from mandatory e-Invoicing implementation.

Relaxation Period for Smaller Businesses

For businesses in the lower revenue tiers, LHDN has introduced a temporary relaxation period to allow additional time for system preparation and process adjustments.

During this period, businesses are expected to take reasonable steps to prepare for e-Invoicing implementation, including reviewing their invoicing workflows and accounting systems.

Submission Methods

Businesses can transmit e-Invoices to LHDN through two main methods:

• MyInvois Portal – suitable for smaller businesses or companies with lower invoice volume

• API Integration – direct connection between a company’s accounting or ERP system and the MyInvois platform

Each method has different operational considerations depending on the size and transaction volume of the business.

Why Businesses Should Start Preparing Early

Although some SMEs may only be required to comply in later phases, preparation is still important.

Implementing e-Invoicing may require businesses to:

• review existing invoicing processes

• ensure accounting systems can generate required data fields

• train staff on new digital compliance procedures

Early preparation can reduce disruption once the mandatory implementation date applies.